What a week this has been for the housing market, from the fireworks of Fed Chair Jay Powell’s Congressional testimony to an attempt to break over a critical line on the 10-year yield. Then Friday we got solid jobs and labor force growth data and the surprising failure of Silicon Valley Bank. Let’s look at each of these, one at a time.

Fed Chair talk

First, Federal Reserve Chairman Jerome Powell did not have his best week as he looked unsure of himself, like most Fed members have recently, about what is happening here with the economy and the path of future rate hikes.

I could spend three days on this topic; however, for the sake of focusing on the jobs report today, I would listen to this podcast and read this article to understand my frustration now with the Fed messages. My entire stance on the Fed not pivoting was based on their logic about why they hiked rates so fast.

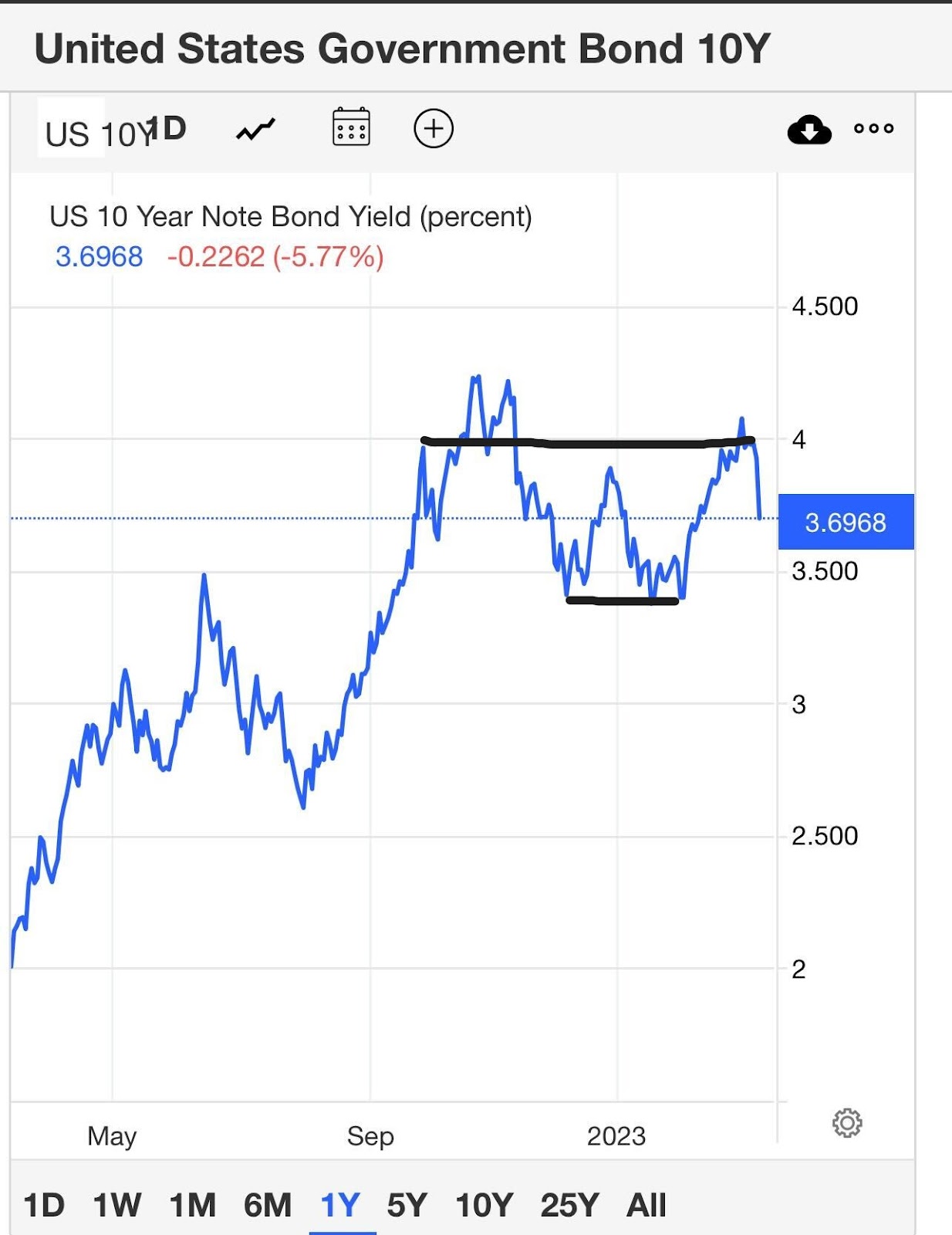

10-year yield

Those following the weekly Housing Market Tracker article already know I have discussed critical technical levels on the 10-year yield on the bottom-end range and where we were this week. It’s going to take something big to break above this level and get to my 10-year yield peak call forecast at 4.25%.

A snapshot of today’s 10’s year yield at this second:

I feel terrible for some of my friends who were livid this week that the 10-year yield didn’t blow up higher with the Fed funds rate being priced higher for longer. However, as I have stressed recently, this isn’t the 1970s baby, and the long end of the bond market is having a “married at first sight” spat with the short end of the bond market for some time now.

Bank run?

The news that Silicon Valley Bank failed has to have shocked Mary Daly, president and CEO of the San Francisco Federal Reserve Bank of San Francisco since this happened in her district. I expect some emergency Fed meetings over the weekend to see if other banks are at risk. Read the statement by the FDIC about taking over the bank here.

Jobs, jobs, jobs

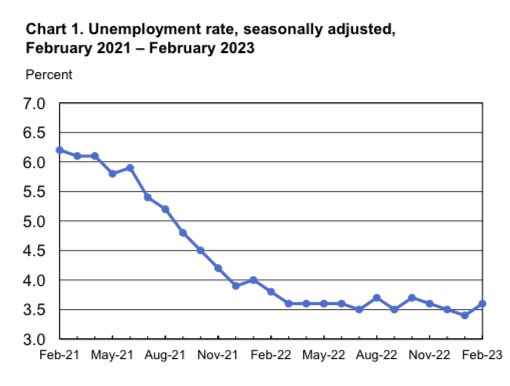

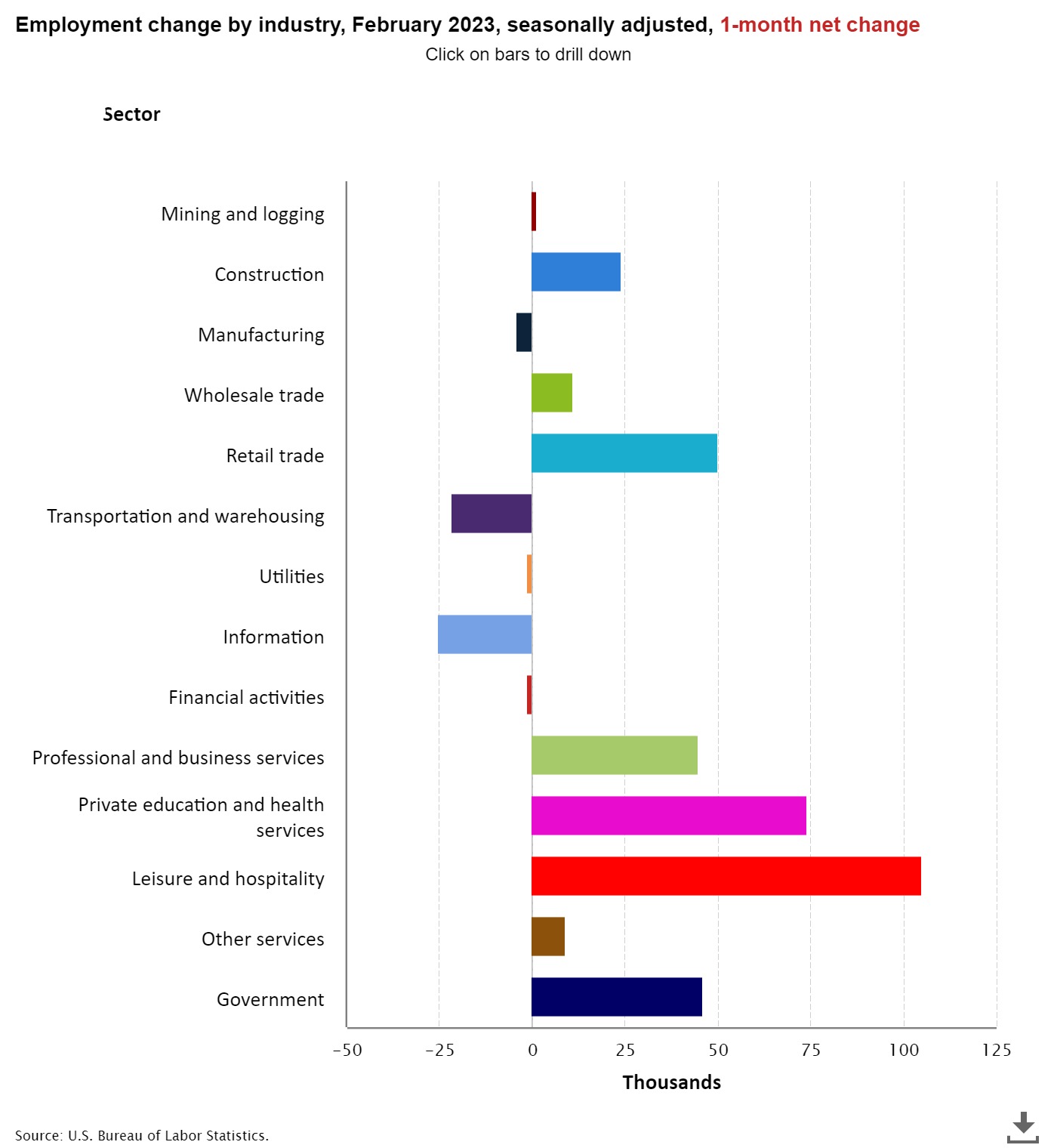

From BLS:Total nonfarm payroll employment rose by 311,000 in February, and the unemployment rate edged up to 3.6 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in leisure and hospitality, retail trade, government, and health care. Employment declined in information and in transportation and warehousing.

How can the unemployment rate increase and we still have big job numbers printed? Well, if the labor force grows, this happens from time to time and this is the Federal Reserve’s dream to have the labor force growth rise faster.

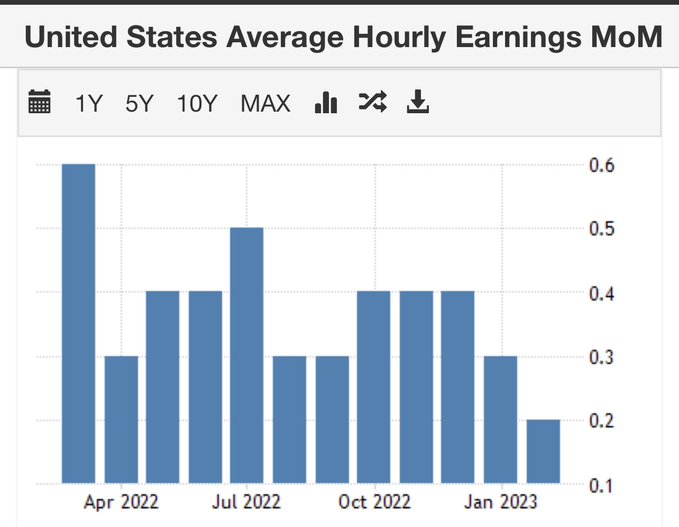

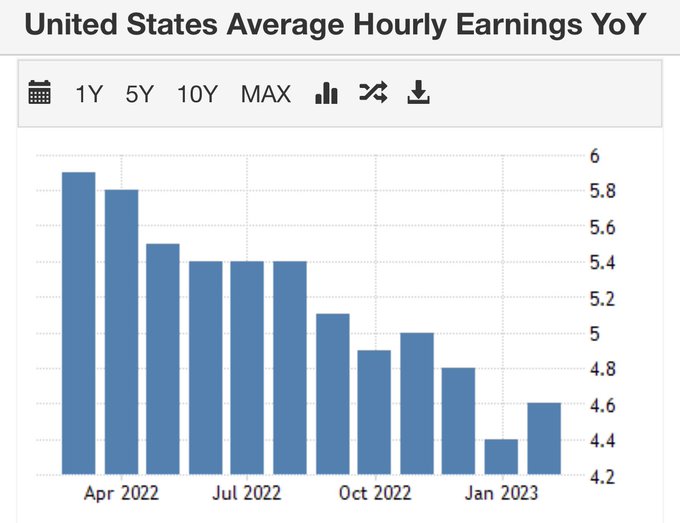

The Federal Reserve wants wage growth to cool down more and more and believes a higher labor force growth will help them.

What the Fed wants is for the wage growth data on a year-over-year basis to head much lower and stay there. According to the Fed, Americans are getting too much wage growth, and labor has power over their bosses — this will not be tolerated in America.

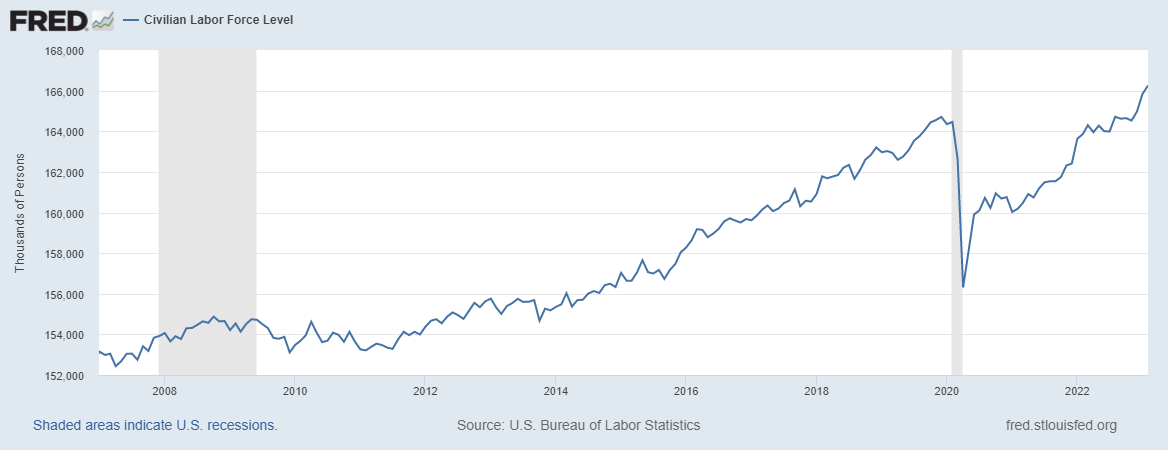

The labor force participation climbed noticeably from prime-age people and is now close to the pre-pandemic highs.

The total civilian labor force level is over 166 million, so we have people who can fill the jobs and get us to the job-growth level we should have had before COVID-19.

For those who did not follow me during the COVID-19 recovery, I had a few critical talking points about the labor market:

- The COVID-19 recovery model was written on April 7, 2020. This model predicted the U.S. recovery would happen in 2020 and I retired it on Dec. 9, 2020.

- I said the labor market would recover fully by September of 2022, which means it would take some time before we could get back all the jobs lost to COVID-19. During this process, I predicted that job openings would get to 10 million. Even in 2021, when job reports were missed badly, I doubled down on my premise.

- Now, depending on how long this expansion goes on, we still are in make-up mode for jobs.

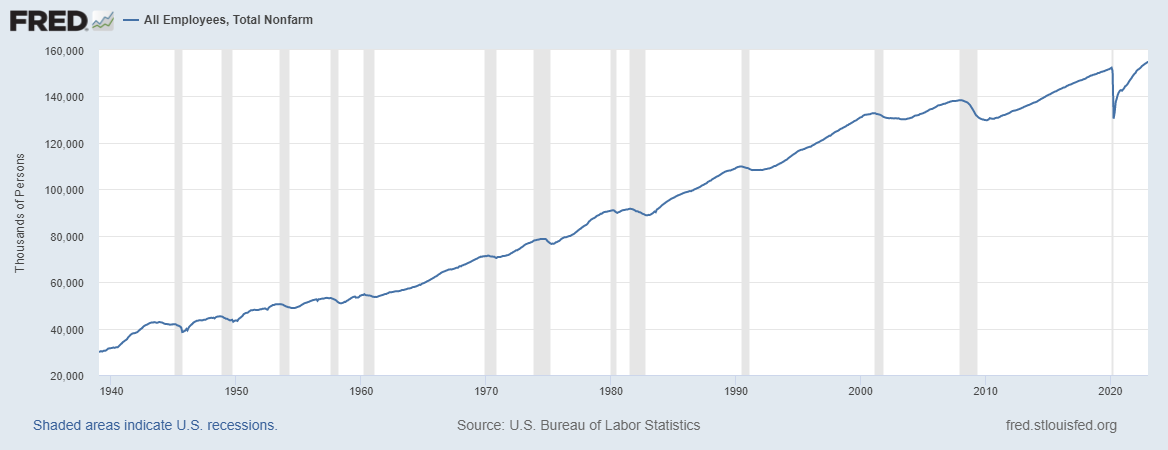

Before COVID-19 hit us, our total employment was 152,371,000. We were roughly averaging over 200K jobs per month back then and in early 2020 labor was improving. So, assume that we had no COVID-19 and job growth continued, with no recession. It’s not a far-fetched premise to say we should now be between 158-159 million jobs, not 155,350,000 jobs as reported today.

The closer we are to catching up, the slower the jobs data growth will be — as long as the economy is expanding. We have a few sectors of the economy laying off workers recently. Below is a breakdown of the jobs gained and lost with Friday’s report. With recent headlines, it’s not a surprise to see jobs being lost in the information and warehousing sectors.

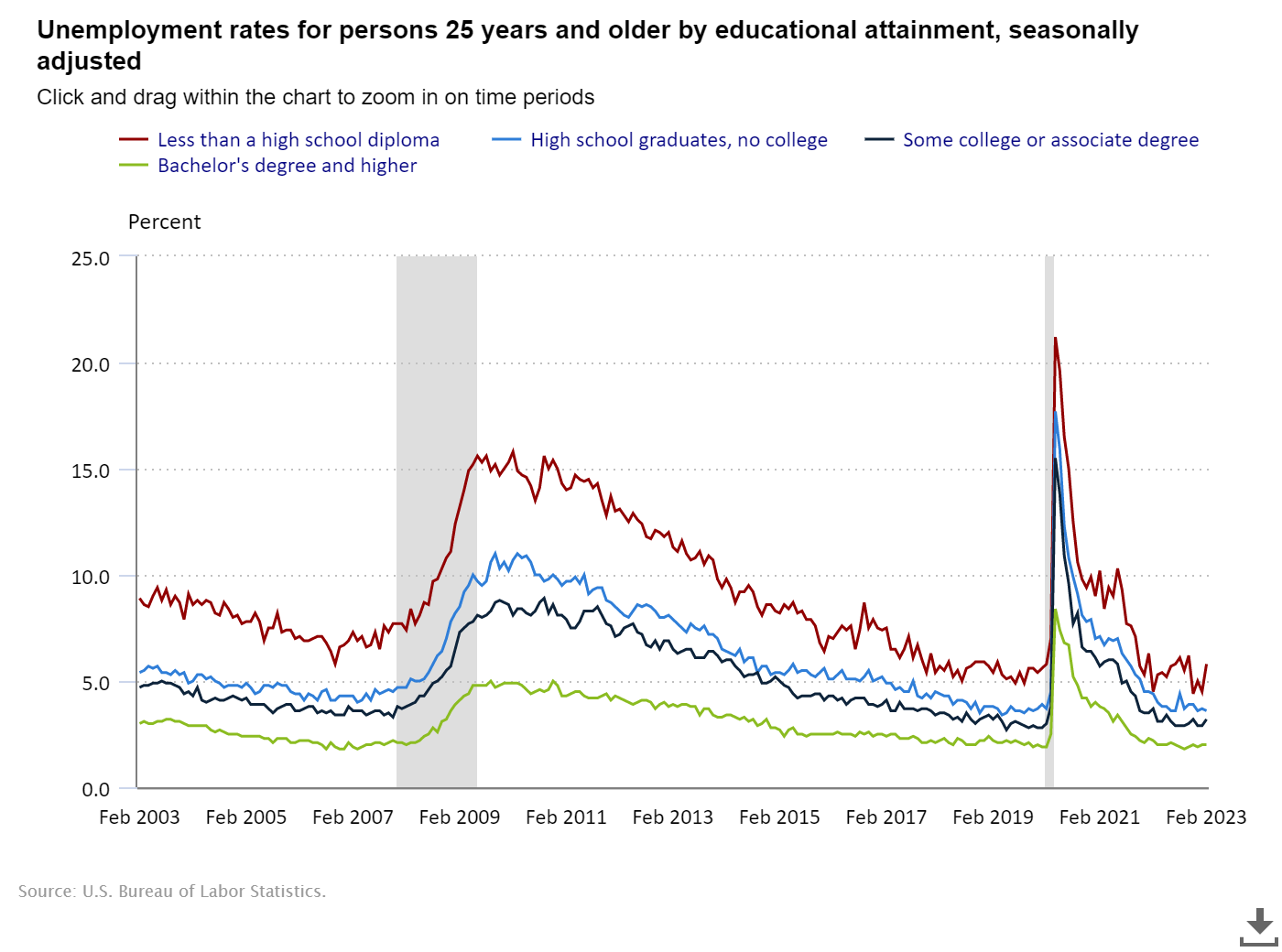

Here is a breakdown of the unemployment rate tied to the education level for those aged 25 and older:

- Less than a high school diploma: 5.8% (previously 4.5%)

- High school graduate and no college: 3.6%

- Some college or associate degree: 3.2% (previously 2.9%)

- Bachelor’s degree or higher: 2.0%

This has been a crazy week — one for the record books for sure. With a lot of jobs and labor data, a bank going under, and the Fed Chair talking to Congress for two days, we can all use a break on the weekend. On Monday’s podcast, I will go into many details about what I thought of this week. However, who knows what the news will be by Monday morning?

I’ll talk about why the bond market has still stayed in the 10-year yield channel in Monday’s Housing Market Tracker. The question is: What will the Federal Reserve do now since market watchers think the Fed will keep hiking until they break something?