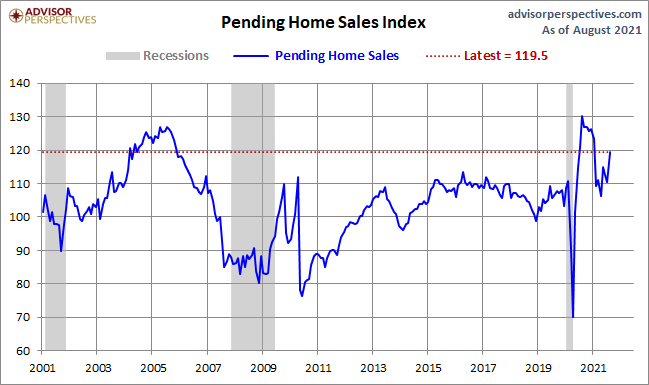

Today’s pending home sales came in at a big beat of estimates, running at 8.1% for this report. More importantly, this data line looks just right. One of my main goals for sharing housing sales data in 2021 is to give people a sales trend range to work off this year to know if home sales are doing well.

Last year we had an abnormal burst of housing demand that was just make-up demand from the COVID-19 pause in the second half of 2020. This led to home sales data surging to levels that were not sustainable and were going to moderate.

My concern was that people would overreact to that sales moderation and not know how to make COVID-19 adjustments to data. As we all know, the housing sector has extremely well-developed yet untalented Americans calling for a housing crash during the years 2012-2021. My job has always been to show you why this wasn’t the case. As someone who has been talking about the years 2020-2024 having the best housing demographics ever recorded in history, a home sales crash in demand wasn’t in the works in 2020 or 2021.

When pending home sales data was fading early in the year, I wrote that pending home sales look just right. The falling of demand is very normal and the housing market is going to find a base to work from and move forward.

“The rule of thumb I am using for 2021 is that existing home sales if they’re doing good, should be trending between 5,840,000 – 6,200,000. This, to me, would be considered a good year for housing. This also means that we should have some prints above 6,200,000 like we have had already and below 5,840,000, which hasn’t happened yet. We ended 2020 with 5,640,000 existing home sales, which was roughly only 130,000 more than 2017 levels.

“I have always stressed the key idea of replacement buyer demand, which runs in line with my mindset that demographics are the best in the years 2020-2024. This means for me that total home sales, both new and existing, combined should be higher than 6,200,000.”

It’s almost October, which means that the 2021 housing collapse crew now would need a massive epic crash in November and December. Good luck, forbearance crash bros, after today’s pending home sales.

From the National Association of Realtors: The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, increased 8.1% to 119.5 in August. Year-over-year, signings dipped 8.3%. An index of 100 is equal to the level of contract activity in 2001.

As you can see below in the chart, housing data, like most economic data, has been wild with the COVID-19 pause and then the massive recovery of demand in a short time. Like my moderation theme was trying to present, we will moderate to find a base and then work there. This is exactly what has happened in 2021, and the sales range has stuck well.

I have been looking for some prints under 5,840,000 to offset the prints over 6.2 million we had during the recovery. However, as of yet, we’ve only had one print under 5,840,000

One key for the rest of the year is that we will see a lot of harmful year-over-year sales data due to the rapid increase in make-up demand in the second half of 2020. Don’t focus on the negative year-over-year data, but focus on trend sales. A few extreme housing bears, some of whom have talked about housing collapse in the second half of 2021, don’t have the educational training to read data correctly. This doesn’t mean you have to join this group; you can think for yourself because your mind is your own — don’t let doomsday cult people manipulate you. Falling lumber prices, survey data showing that it’s the worst time to buy a home, home prices overheating and forbearance all have been used as marketing gimmicks to say housing is on the verge of a collapse in 2021.

It didn’t happen; not only did it not happen, 2021 home sales are going to be higher than 2020 levels. It was bad enough these people whiffed from 2012-2019, especially in 2018. Then they believed COVID-19 was their savior on bad housing crash calls in 2020. Just because this crash cult can’t just shut up, they went for it 2021. All I can say is, let their forecasts speak for themselves. It has been nothing but an epic disaster for one of the most significant crash cult groups in modern-day history, the housing bubble boys of America.

This is why last year I wrote that home sales were going to be positive, that these people aren’t trained to talk about housing economics. “Years 2020-2024 have a healthy number of replacement buyers as our most significant housing demographic patch ever recorded in history (Ages 26-32) comes into their home-buying age. If you think of these Americans as replacement buyers, then 2020 makes a lot of sense right now.

“Personally, the housing bears for many years never talked about demographics coherently, and all had a bond market bubble conspiracy theory. These people are wild; we don’t have any other way to explain this kind of logic with the bond market after 40 years. I look at them as older men drunk at a bar going on their iPhone typing in the word bubble.”

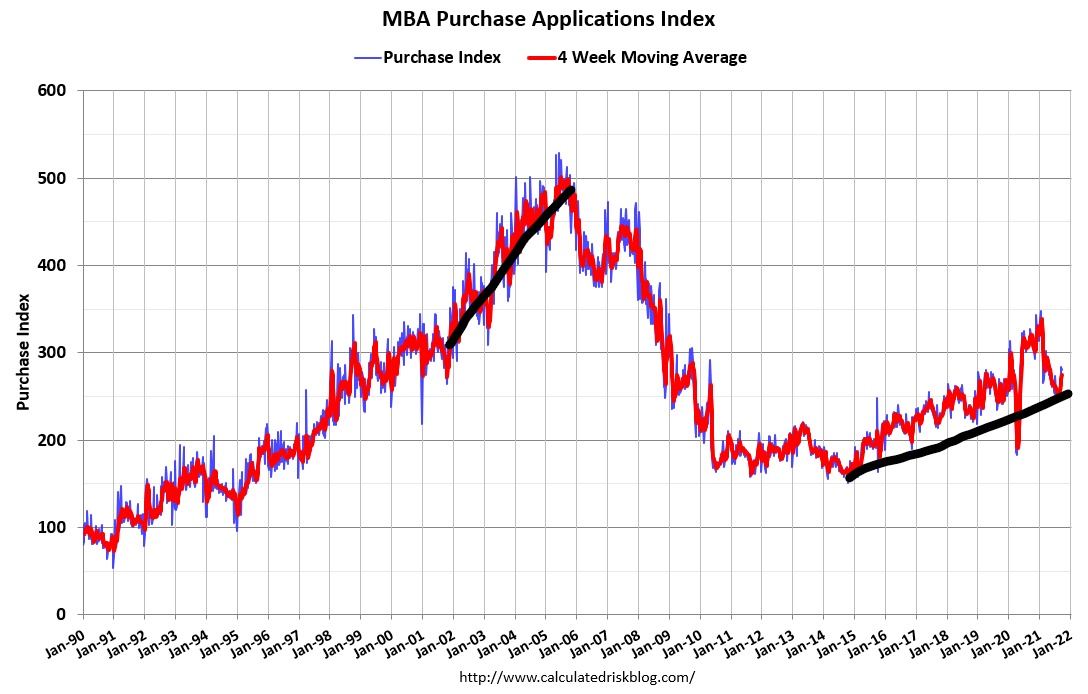

We can safely say that it’s time to move the crash to 2022 (*snicker). Purchase application data, where you can see seasonality kicking in after May, has been firm once you make COVID-19 adjustments. As I wrote early in the year, this data will show negative year-over-year data, but don’t overreact to that reality. Purchase application data found its base and is now moving off that. Talk about insult to injury here with housing data toward the end of the year.

All in all, pending home sales look just right, just like existing home sales data. If you see a forbearance crash bro, hug him and tell them don’t worry, there’s always next year, kid.