The CPI data released today shows the growth rate of inflation cooling off, and that’s good for mortgage rates. If inflation were running hot like in the 1970s, mortgage rates would have easily gotten to 8%-10% last year. The fact that the growth rate of inflation has been falling over the last few months is a positive story for mortgage rates over the long run.

Let’s dig in to where mortgage rates are headed.

As shown below, the 10-year yield channel for 2023 aligns with my forecast for bond yields and mortgage rates. The chart also shows that we had lower rates when the inflation growth rate was at its highest recently. This surprised many people because they were looking at the inflation data driving mortgage rates instead of where the 10-year yield was going.

The 10-year yield and mortgage rates have done a slow dance together since 1971, moving in tandem. Recently they have drifted apart because the mortgage market is stressed, but they’re still bound to each other. I always look at where I believe the 10-year yield will range in a year and the inflation growth rate wasn’t the main driver this year: It was the labor market.

Last year the bond market had a crazy ride while trying to digest all the Federal Reserve rate hikes and dramatic world events. In addition, the inflation growth rate was the highest in recent history last year while the 10-year yield was lower than mortgage rates. That can be confusing, but sometimes the growth rate of inflation isn’t the main driver of mortgage rates.

In my 2023 forecast, I said if the economy stays firm, the 10-year yield range should be between 3.21% and 4.25%, equating to mortgage rates between 5.75% and 7.25%. Of course, the spreads with the mortgage rate and the 10-year yield have worsened since the banking crisis, which is the big story of 2023. However, outside of that, the 10-year yield looks right as the labor market hasn’t broken yet and the inflation growth rate is falling. I define the labor market breaking as jobless claims getting over 323,000 on the four-week moving average, and we aren’t there yet.

The CPI data

The CPI data from BLS: The Consumer Price Index for All Urban Consumers (CPI-U) rose 0.2 percent in June on a seasonally adjusted basis, after increasing 0.1 percent in May, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 3.0 percent before seasonal adjustment.

The headline inflation growth rate is slowing down as everyone anticipated, and if any Fed member says no progress has been made on inflation, I need to come up with a term stronger than old and slow. The growth rate of headline CPI has collapsed, as you can see in the chart below.

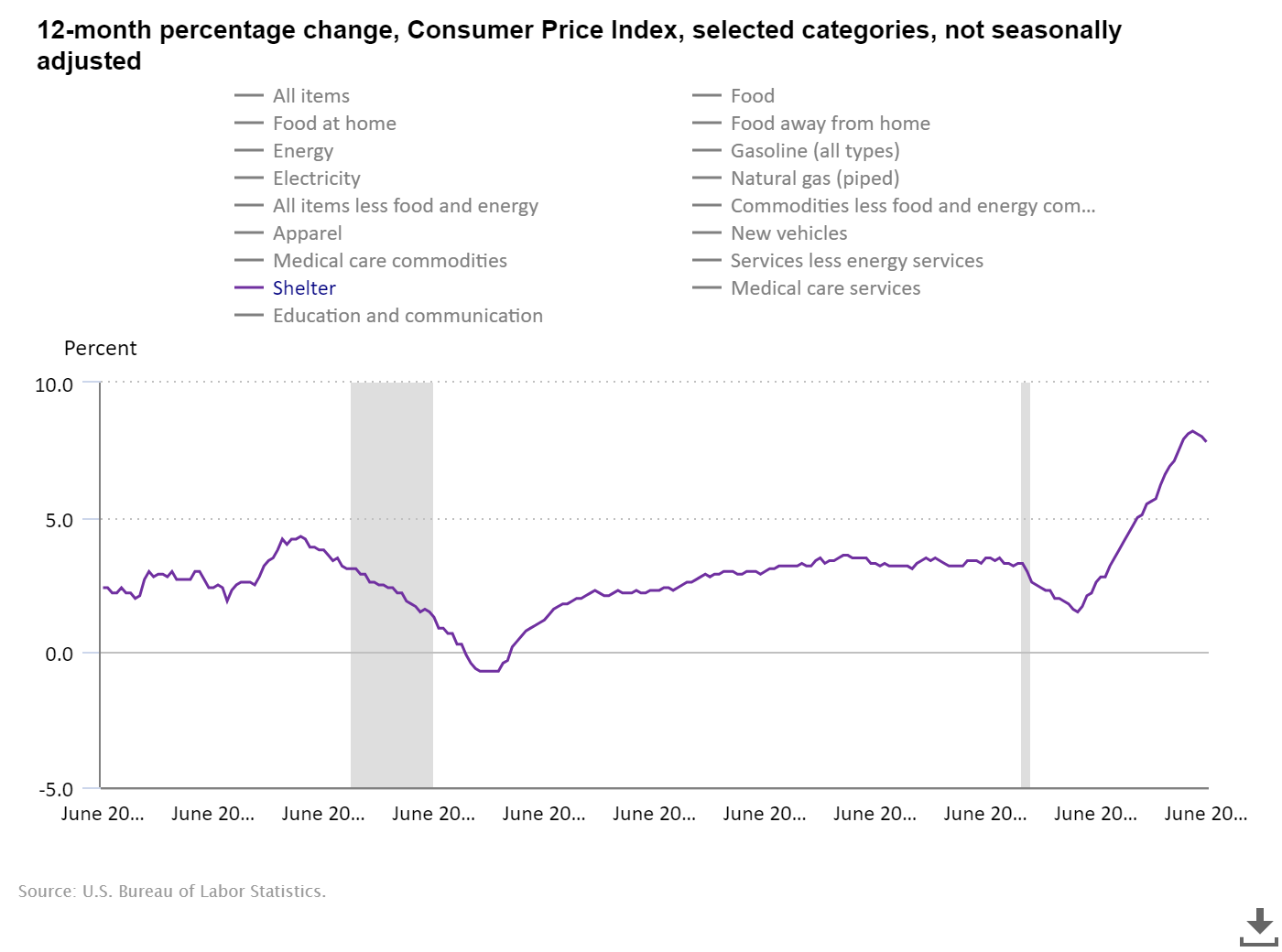

Last year on CPI day in September, I went on CNBC to explain that the shelter inflation portion of CPI data, which is 44.4% of the weighting, was going to lag reality and that in 2023 it would be a positive story as the growth rate of inflation would cool. We are now seeing this process take its course, which will help cool down core inflation over the next 6-12 months.

In real time, the biggest component of core CPI — shelter — is already cooling off, but it’s still lagging in the data.

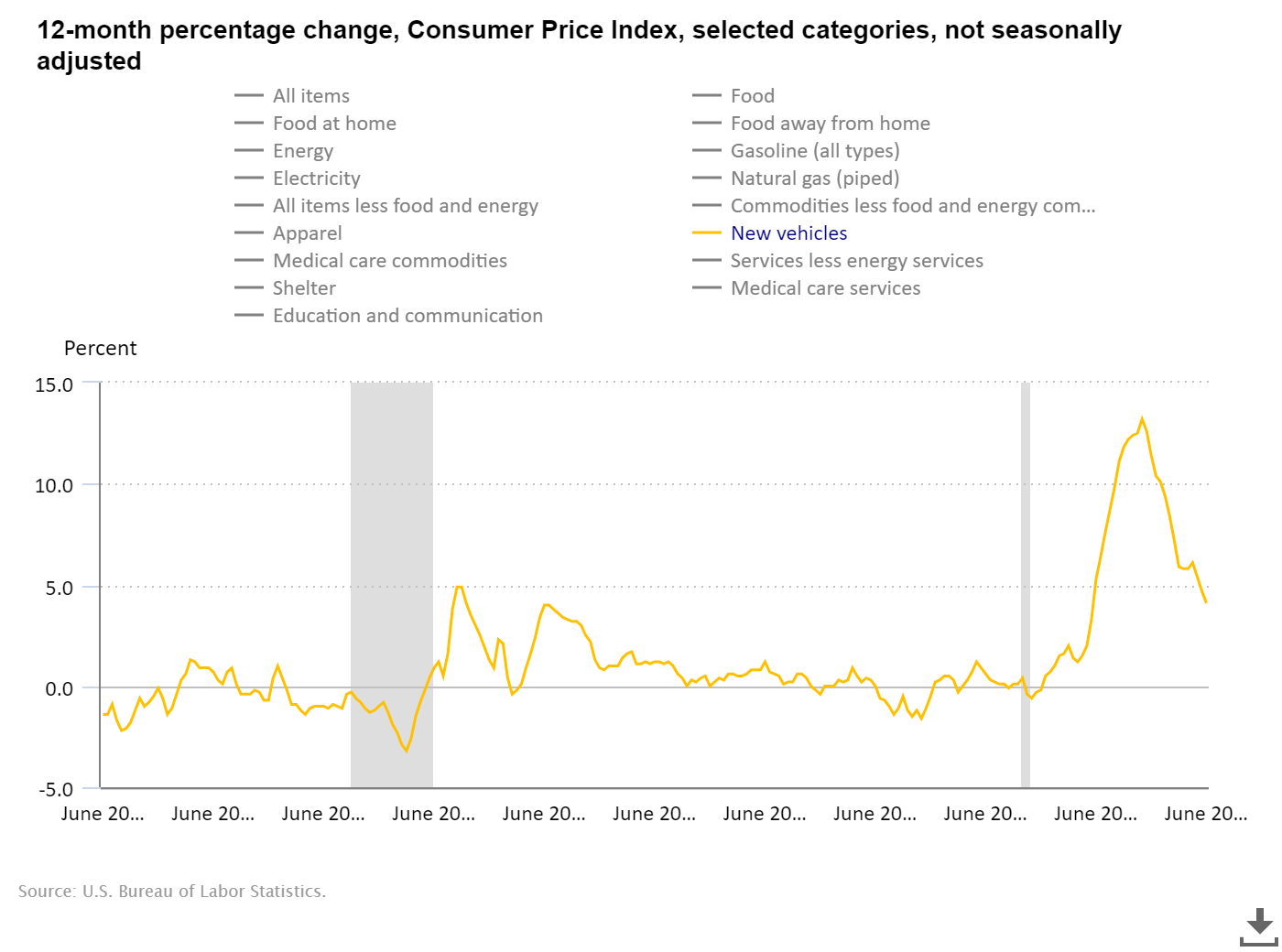

The most frustrating inflation aspect has probably been car prices: the shortage of chips and supply of cars boosted inflation because of the pandemic lags and other issues. However, the growth rate of car inflation is falling and the used car price index should be cooler over the next few months, which will help. We now have two positive stories looking out 6-12 months on core inflation which will cool the growth rate of inflation down.

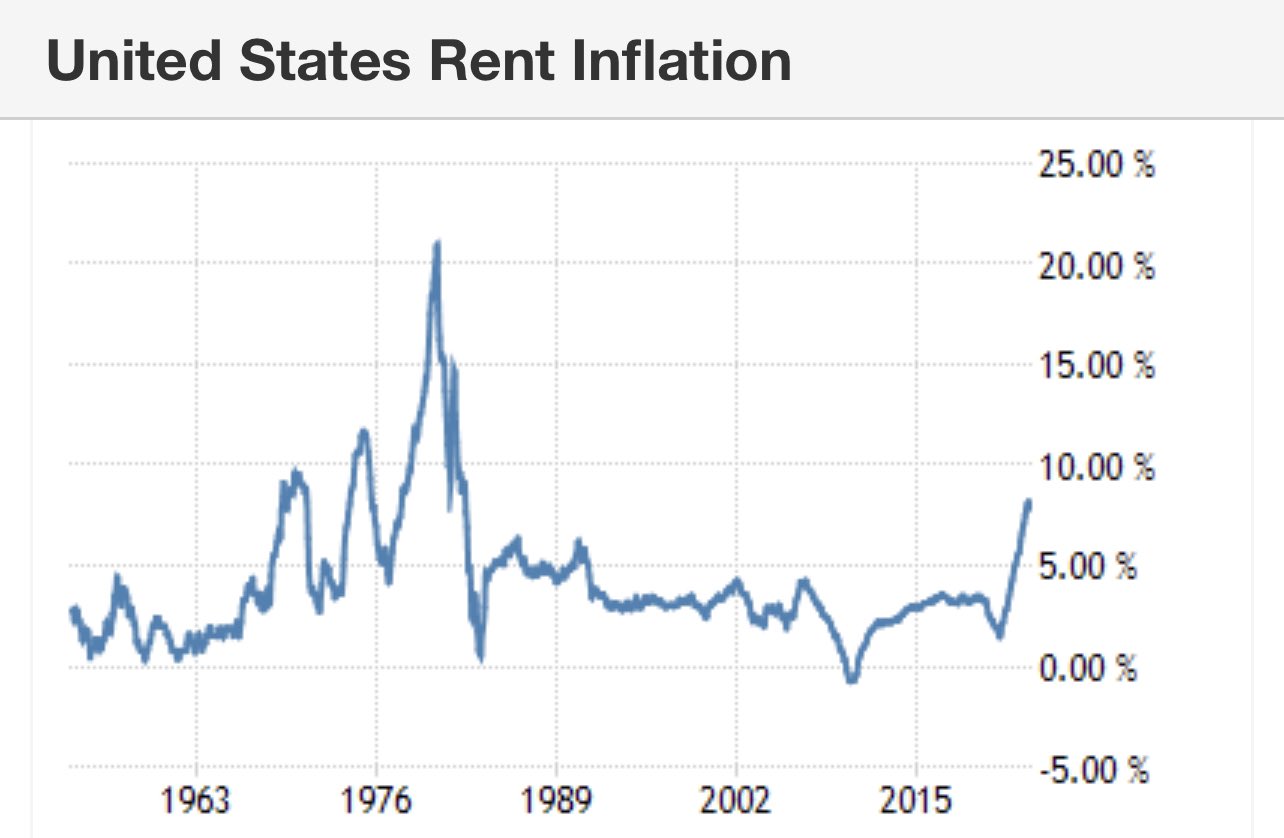

All in all, today’s report is positive but one that the markets have expected for some time. If inflation was taking off like the 1970s as the Fed fears, rent inflation would be skyrocketing and honey, that story is dead.

The Federal Reserve over-hiked for no reason the last three rate hikes and if they hike again, the only purpose at this stage would be to target American workers so they lose their jobs. But the 1970s are dead, and the Fed doesn’t need to create a job-loss recession to bring down the inflation growth rate. The Fed needs to endure, let the supply side of certain items come to place and not crash the plane.

If you wonder why the Fed is still talking about more rate hikes with all the data we have now, the best answer I can give you is this: The Fed believes it needs to make real yields higher. As the inflation growth rate falls, it is being more restrictive, which will help it get the unemployment forecast of 4.5%. If it seems like they want to hike more or not even talk about cutting rates, that’s because it was always about attacking the labor market, which is still too strong for them.

Appreciate your insights Logan

Robert A.