Are we headed to a housing bubble? The Dallas Fed on Thursday published an article titled: Real-Time Market Monitoring Finds Signs Of a Brewing U.S. Housing Bubble. The online reaction was immediate — housing must be about to crash. I disagree with this conclusion. That’s not to say that the data points the Fed used are incorrect — in fact, we are in a savagely unhealthy housing market, but it’s not a bubble.

Let me explain.

First, because there is no speculative debt demand going on today, there can’t be a housing bubble. We aren’t anywhere close to the housing bubble dynamics we had from 2002 to 2008; that environment is simply impossible to replicate.

My rule of thumb has always been, if you’re going to use the phrase housing bubble, you need to point to when the bubble started, because a bubble means that prices would fall back to some earlier point in time. For the housing bubble 2.0 crew, this would mean home prices would have to get back to 2012 in a short amount of time.

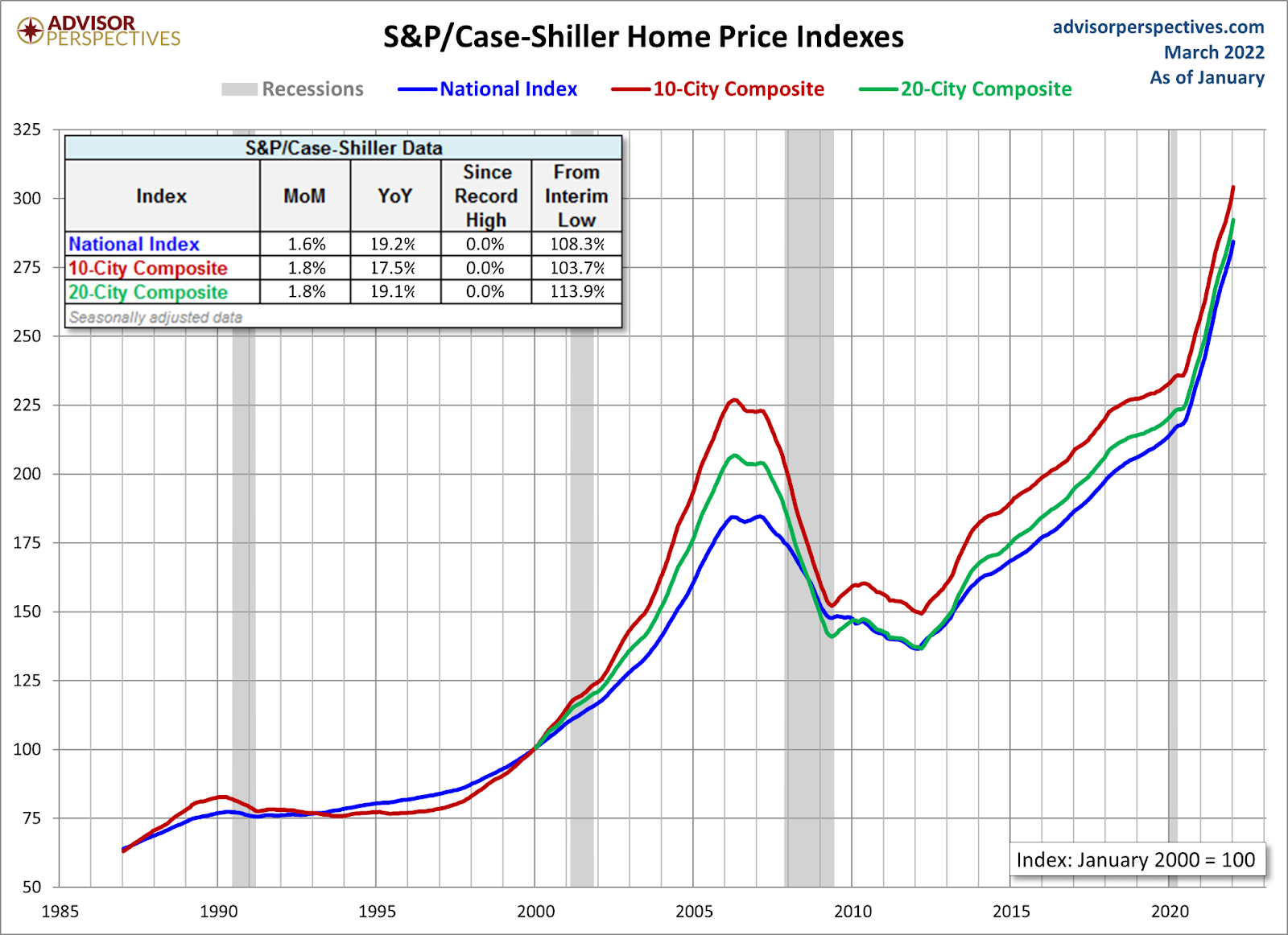

Home prices have grown 108.3% since the 2012 lows and that is the magnitude of decline we would need to see to justify using the term “housing bubble.” The notion that educated homeowners with positive cash flow — who aren’t showing any stress in making their low payments thanks to historically low mortgage rates — would sell at 50%, 60% to 70% off current values and go back to renting, doesn’t seem realistic. Especially in a year when inventory has crashed to all-time lows and demand for those houses is still so high.

The people at the Dallas Fed aren’t cheap professional troll artists with terrible housing YouTube crash videos, so what’s going on? I’m going to take their talking points and explain in detail why this isn’t the housing bubble of 2002-2005.

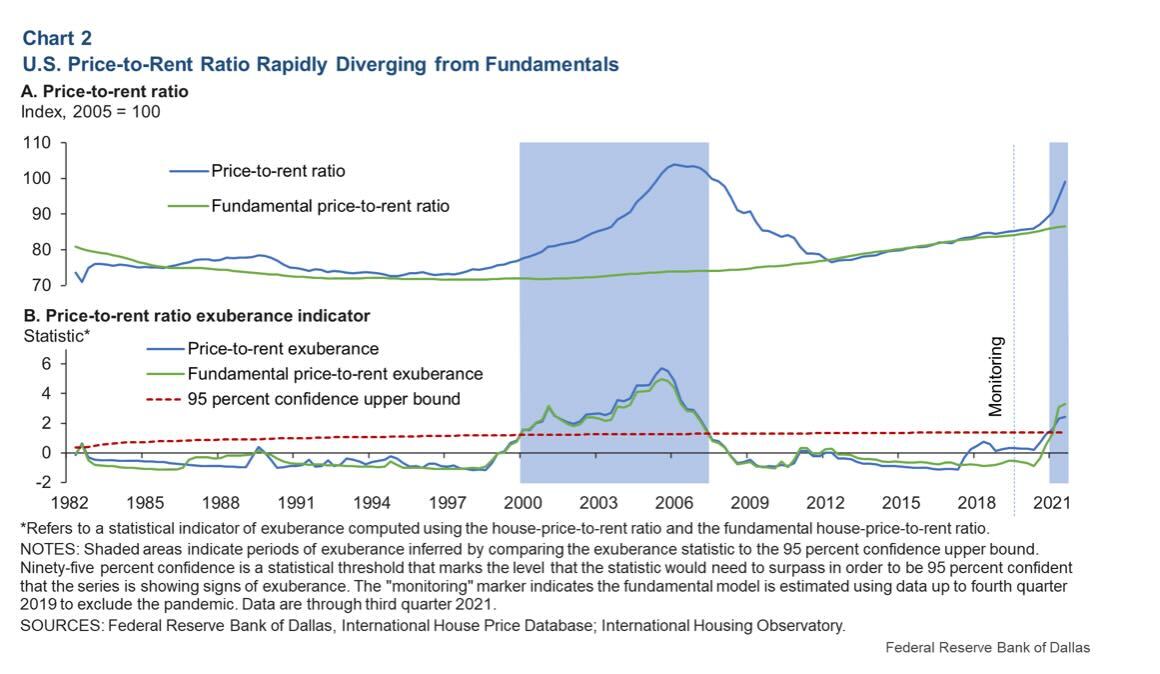

“Our evidence points to abnormal U.S. housing market behavior for the first time since the boom of the early 2000s. Reasons for concern are clear in certain economic indicators—the price-to-rent ratio, in particular, and the price-to-income ratio—which show signs that 2021 house prices appear increasingly out of step with fundamentals.”

I agree with this statement and they’re actually calmer about it than I am. I went from calling this an unhealthy housing market to a savagely unhealthy housing market because of price growth. I set a cumulative price growth model of 23% for five years. This got smashed in two years, and inventory levels broke to all-time lows this year. So, for me, I need pricing to be flat to negative this year, next year, and in 2024 just to keep that 23% price model in check. They’re just highlighting what I have been saying for some time: home price growth is too hot.

In reality, the Dallas Fed and I may have different talking points, but we are saying the same thing: home price growth is too hot. But, importantly, home prices getting too hot doesn’t create a bubble. A housing bubble does have robust demand, but it’s speculative demand. Once the drivers of that speculation fall out, demand just collapses. Today, people aren’t buying homes because they are speculating that home prices will increase double digits each year, they’re simply buying a home to live in for a long time.

“Based on present evidence, there is no expectation that fallout from a housing correction would be comparable to the 2007–09 Global Financial Crisis in terms of magnitude or macroeconomic gravity. Among other things, household balance sheets appear in better shape, and excessive borrowing doesn’t appear to be fueling the housing market boom.”

Given the above statement about homeowners’ balance sheets and the fact that we don’t have excessive borrowing, the headline about a housing bubble brewing is an overreach until we see those factors come into play.

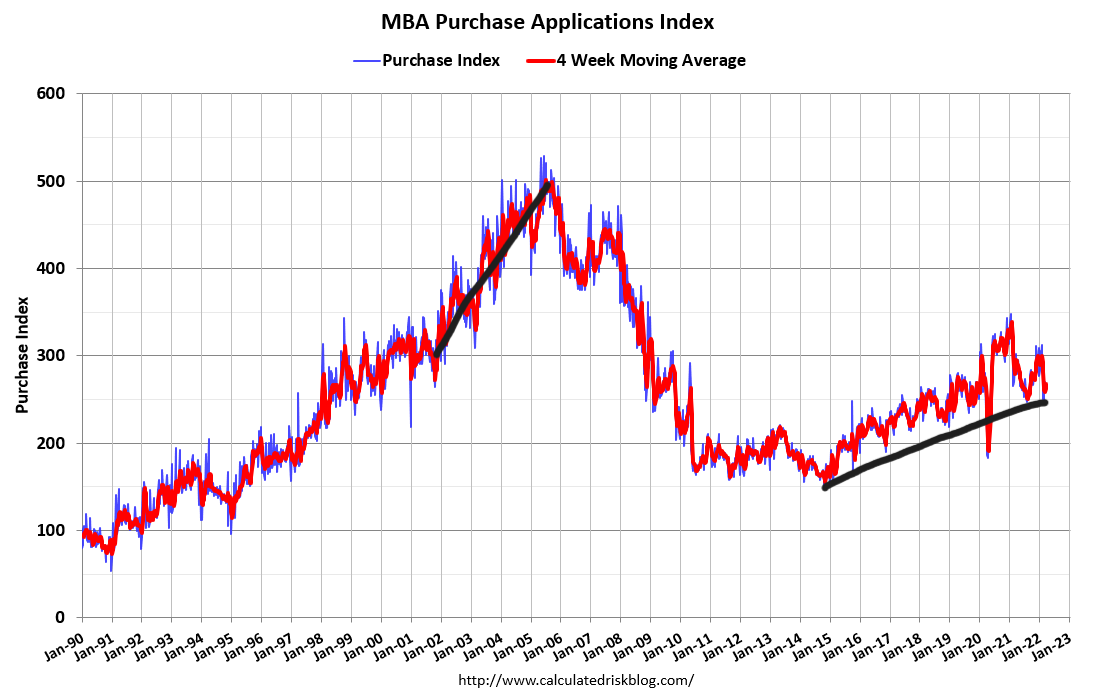

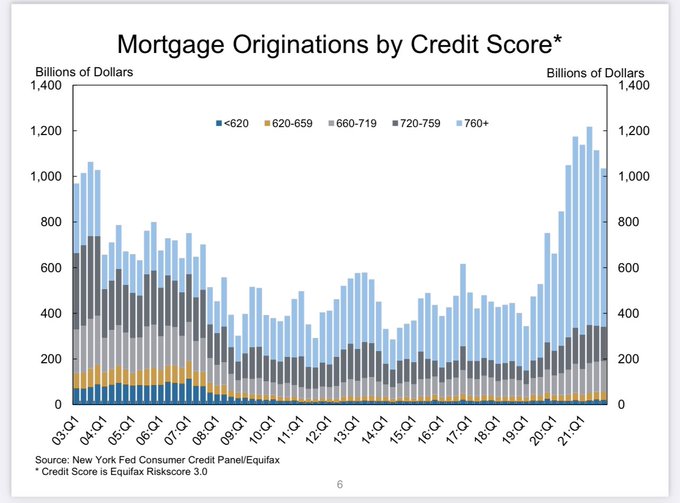

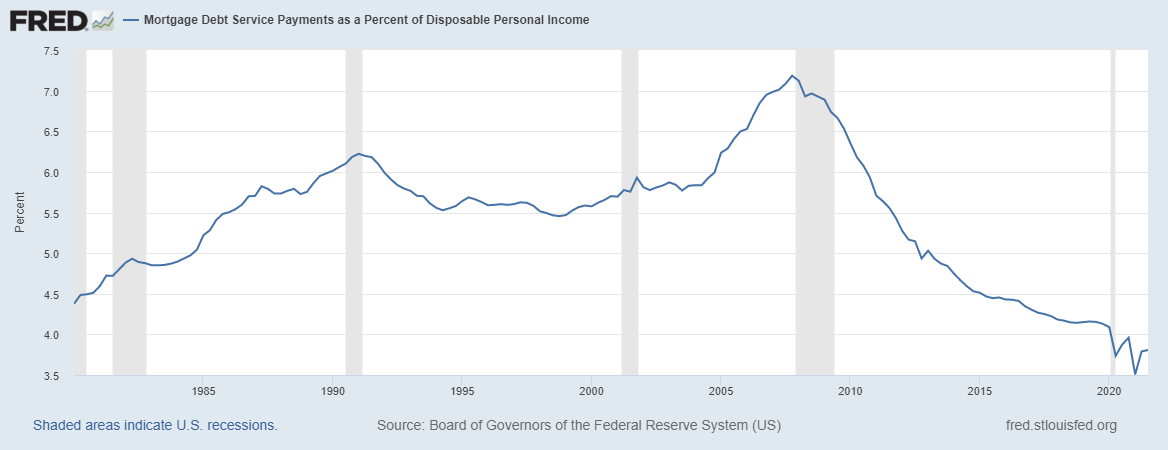

Over the years, I have tried to express that we won’t have a repeat of 2002-2005 when it comes to a speculative mortgage debt expansion on unsound credit. Instead, homeowners have the best financial profile in America’s history. This is why I like to show the MBA mortgage purchase application chart. Yes, it had a 1% growth week to week, but as you can see, even with this week’s data, we aren’t seeing a credit boom in America. The speculative debt boom we saw from 2002-to 2005 can’t be repeated with the current lending standards in place. This is a good thing, it protects us well in downturns.

Remember that the forbearance crash bros got it so wrong because they never took into account the balance sheets of American households, which are fantastic. Fixed low debt cost with rising wages creates better cash flow

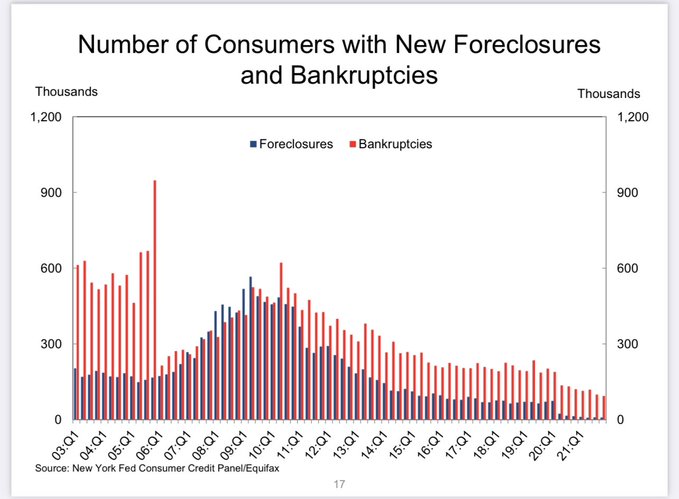

Post-2010, the lending standards have been great — we made American mortgage debt great again! In the past, the speculative credit boom led to people filing for bankruptcies and foreclosures in 2005, 2006, 2007 and 2008. Then after all that, we had the great recession.

Things are much different this time around. When you have a great credit profile, you don’t see a surge in credit stress right before the recession.

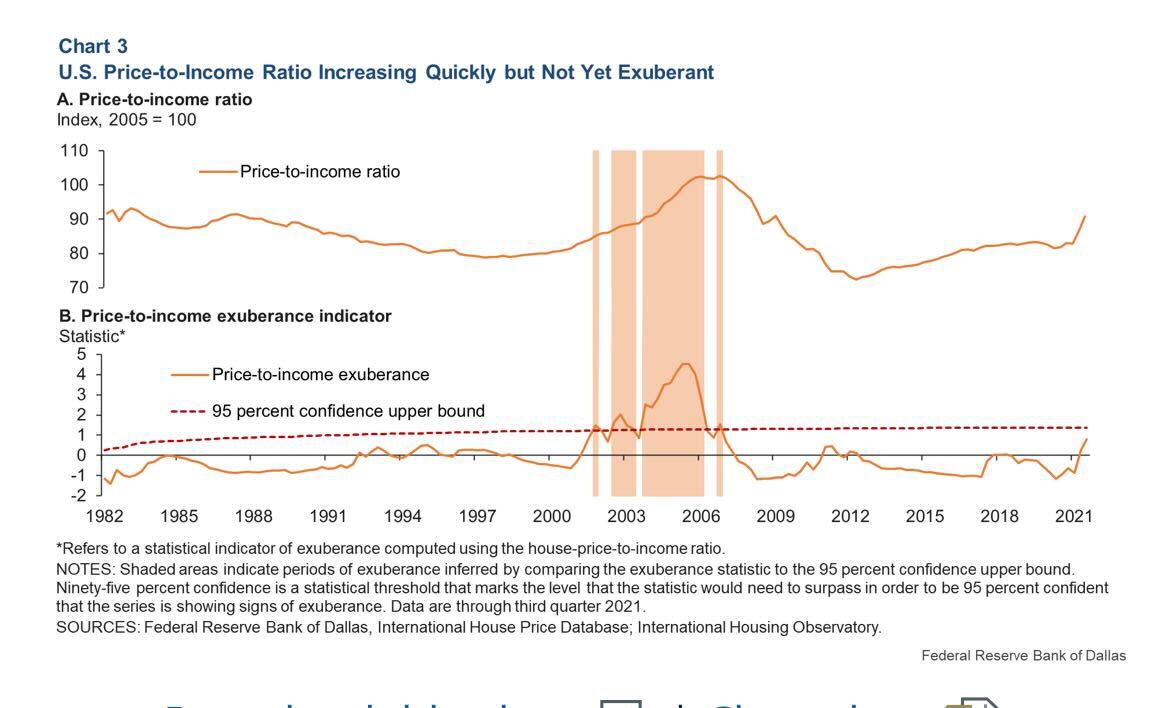

Another important long-run anchor—tied directly to housing affordability—is the ratio of house prices to disposable income. Chart 3 shows dates of episodes of exuberance for this measure of housing affordability. These data—unlike our previous metrics—do not yet display evidence of explosiveness in the third quarter of 2021. But the rapid increase in the statistic close to the threshold during 2021 indicates that U.S. real house prices may soon become untethered from personal disposable income per capita.

I believe the Dallas Fed is really stating the obvious here that home prices have gotten too hot lately and we need to be mindful of this. Of course, I’ve been saying we need higher rates to cool down the marketplace. I don’t see anything wrong here with what they’re saying or the models they’re using. Heck, I am talking about using credit controls if higher rates don’t calm down-home price growth, so in that way, the Dallas Fed is much more diplomatic than I am. But again, rising prices by themselves don’t lead to a bubble, you need excessive speculation, as they have noted.

All in all, I liked the piece from the Dallas Fed and I believe people should read it. Many people might come away with different takes, but I came away with one take, which is the same thing I have been saying: The housing market has gone into a savagely unhealthy stage because inventory is too low and the forced bidding action is creating too much price growth.

Sometimes people see a headline with the word bubble in it and everyone goes straight back to 2008. Well, 2008 wasn’t really about 2008, it was the marketplace from 2002 to 2008, which clearly is something we don’t have right now in housing. I believe the Dallas Fed explained that to a small degree.

Each economic cycle is unique with its own set of new variables. Of course housing in the years 2020-2024 means something to me because it’s been a period of time that I have been focusing on. Of course, nothing goes as planned: COVID-19, the Russian Invasion of Ukraine and the lack of goods to build homes in a timely manner are all new variables. We just had to take the data one day, one week, and a month at a time and try to find out where the market is going. Right now, that’s not a bubble.

I agree with all this. One metric I don’t see anyone publishing or speaking about is the amount of money in the marketplace by investors / Hard Money Loans.

This wasn’t as popular pre Great Recession era and very popular now.

Would like to see how this is impacting the current market.

This article is quite remarkable and so well-rounded.

You discount fact that consumer balance sheets strong due to government stimulus programs such as rent moratoriums, mortgage forbearance (forbearance on all sorts of debt during pandemic), historically low debt payments for those actually paying their debt, PPP & EIDL loans that nobody has had to start paying back yet. All these stimulus programs are over and can’t come back (even if we have another macro shock) due to the inflation we’re dealing with right now.

What happens when companies start hiring overseas to address the shortages in labor talent pool? WFH won’t seem like such a great idea when your job gets outsourced to someone who will fill your white collar position for 30% of what you are paid. Once companies figure out they can avoid paying expensive office space and hire for less how will that effect unemployment levels?

You always talk about low inventory but I don’t really hear good analysis re: why that’s happened or if it will continue. Saying prices are high and will continue to be high because inventory is low isn’t really analysis it’s more just reporting. Obviously inventory low (demand > supply) when prices are going up but that is an effect not a cause. The Dallas Fed article was saying that people are buying not because it makes financial sense but because they fear that if they don’t purchase now they will miss out (FOMO) and they were asserting this is a form of speculation. Buying that isn’t tethered to fundamentals but on a hope and a prayer that the investment will go up is speculation. I guess your argument is that since inventory is low and demand is high the fundamentals are good but I think if you look at the factors that got us to where we are today and ask if they will continue its fair to question whether the trends of the past are sustainable. You should be a little more humble in your condescension re: the people who have thought housing was going to crash. Did you “predict” that housing was going to spike during pandemic because of govt increasing money supply and fiscal stimulus?

It doesn’t matter how high someone’s credit score was, how much they were making at close of escrow or how big their down payment was if economic conditions change and they lose their ability to service their debt

You say wages are rising but aren’t “real wages” in decline due to inflation?

https://www.cnbc.com/2022/02/10/inflation-eroded-pay-by-1point7percent-over-the-past-year.html

https://www.bls.gov/news.release/realer.htm

I think most people are buying property now as a hedge against inflation. But how does that work for multi-family property in big cities with rent control? LA-NY-San Francisco (Los Angles is still in a state of emergency due to the pandemic They haven’t ended their rent moratorium yet and likely won’t anytime in the near future as politicians are scared it will make homeless crisis worse)