Homeowners with mortgages continue to see their equity increase in their home, according to the Q2 2017 Home Equity analysis from CoreLogic, a property information, analytics and data-enabled solutions provider.

Home equity for all homeowners with a mortgage, about 63% of total homeowners, increased a total 10.6% annually, or $766 billion since the second quarter of 2016, according to the report.

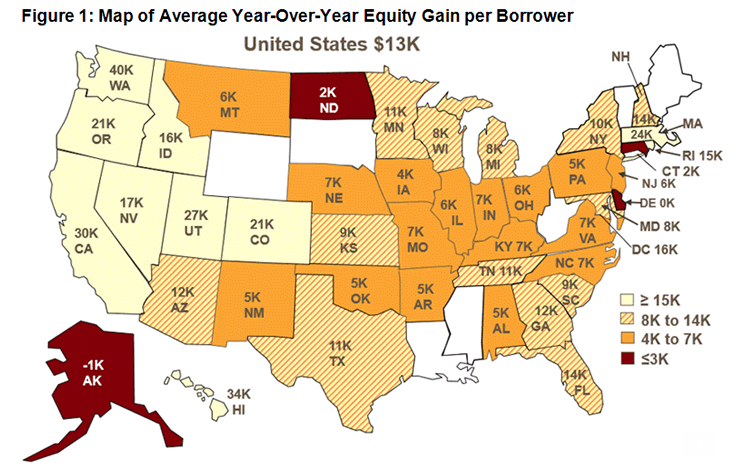

Individually, homeowners earned an average $12,987 in equity between the second quarter of 2016 and the second quarter of this year. Western states saw even higher increases with average homeowners in Washington gaining $40,000 in equity and those in California gaining $30,000 since last year.

The map below shows which states saw the largest rise in equity from the second quarter last year to the second quarter of 2017.

Click to Enlarge

(Source: CoreLogic)

“Homeowner equity reached $8 trillion in the second quarter of 2017, which is more than double the level just five years ago,” CoreLogic President and CEO Frank Martell said. “The rapid rise in homeowner equity not only reduces mortgage risk, but also supports consumer spending and economic growth.”

CoreLogic explained these increases are driven by ever-increasing home prices across the U.S. The most recent House Price Index from the Federal Housing Finance Agency showed home prices jumped 6.3% from July 2016 to July 2017.

And as more homeowners gain equity in their home, the total number of mortgaged residential properties with negative equity decreased 10% from the first quarter to 2.8 million homes. This represents 5.4% of all mortgaged properties. This drop is even more drastic from last year as it fell 21.9% from 3.6 million homes in the second quarter of 2016, or 7.1% of all mortgaged properties.

“Over the last 12 months, approximately 750,000 borrowers achieved positive equity,” CoreLogic Chief Economist Frank Nothaft said. “This means that mortgage risk continues to decline and, given the continued strength in home prices, CoreLogic expects home equity to rise steadily over the next year.”

Negative equity, often referred to as being underwater or upside down, applies to borrowers who owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in home value, an increase in mortgage debt or both.

The national value of total negative equity decreased slightly to $284.4 billion by the end of the second quarter of 2017. This is down $700 million or 0.2% from $285.1 billion in the second quarter last year, but up $200 million or 0.1% from $284.2 billion in the first quarter.