JPMorgan Chase & Co. (JPM) is set to bring another prime jumbo residential mortgage-backed securitization to market in the coming weeks.

Over the course of the year, JPMorgan has brought RMBS transactions to market in varying forms.

Its first jumbo RMBS of the year was backed by fixed-rate, 30-year mortgage loans.

J.P. Morgan Mortgage Trust 2014-1 was comprised of 412 first-lien mortgage loans with an aggregate principal balance of $356 million.

Its second jumbo RMBS of the year was backed by 15-year fixed notes. That offering was built on a pool of 544 loans with an aggregate loan balance of $303.75 million. The offering, called J.P. Morgan Mortgage Trust 2014-2, contained loans with an average balance of $558,361 and has a weighted average loan-to-value of 61.8%.

And late last month, JPMorgan broke new ground with a jumbo RMBS backed entirely by hybrid adjustable-rate mortgages.

J.P. Morgan Mortgage Trust 2014-IVR3 was backed by a pool of 551 loans with an aggregate loan balance of $483.56 million, and each of the loans is a 30-year ARM in various forms.

Three individual sub-pools of loans made up the aggregate loan pool. Pool 1, which represented 8.6% of the total pool, was built on 5/1 ARMs. Pool 2, which represented 58.8% of the total pool, consisted of 7/1 ARMs. And Pool 3, which represented 32.6% of the total pool, was comprised of 10/1 ARMs.

The latest offering is built on the more traditional 30-year, fixed-rate mortgage loan.

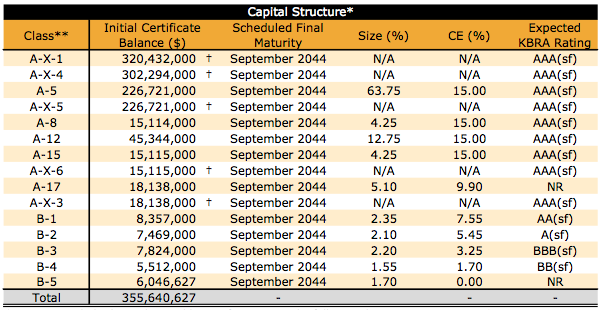

J.P. Morgan Mortgage Trust 2014-OAK4 built on a pool of 434 loans with an aggregate loan balance of $355.64 million. The offering contains loans with an average balance of $819,448 and has a weighted average loan-to-value of 73.7%.

JPMMT 2014-OAK4’s weighted average LTV is higher than in JPMorgan’s previous offerings. JPMMT’s previous high in LTV ratio was 69.4%, which was for J.P. Morgan Mortgage Trust 2013-2.

Both Kroll Bond Rating Agency and DBRS have weighed in on the offering with presale reports, and KBRA says that the LTV ratio is a potential negative for the deal.

“The JPMMT 2014-OAK4 collateral pool consists of high quality, prime mortgage loans that exhibit substantial borrower equity,” KBRA said in its presale report. “While the 73.7% weighted average first- lien loan-to-value ratio and the 74.0% WA first- and junior-lien combined LTV are higher than any other RMBS transaction previously rated by KBRA, they do provide a margin of safety against potential home price declines.”

Click the image below for KBRA's presale ratings.

On the other hand, DBRS cites the quality of the underlying borrowers’ credit scores as a positive of the deal.

“The weighted-average borrower current FICO score of 756 indicates strong borrower credit profiles,” DBRS said. “Approximately 15.0% of the loans have FICOs lower than 720, and 5.1% have FICOs of 800 or higher.”

According to DBRS’ report, the underlying mortgage loans were originated by RPM Mortgage (21.8%), Opes Advisors (16.1%), Homestreet Bank (9.2%), Stonegate Mortgage (5.8%) and other originators that each comprise less than 5% of the mortgage loans.

KBRA cites that several of the deal’s loan originators have limited performance history as a concern for the deal.

“While originator diversity is common and may help reduce geographic concentration, it also increases exposure to the underwriting standards and processes of originators with limited jumbo mortgage loan performance history,” KBRA said.

“Differences in loan origination processes, or in the operations and infrastructure among loan originators, may cause divergent performance outcomes in RMBS pools that otherwise have similar loan characteristics. In addition, some of the originators may lack sufficient financial resources to fulfill their repurchase obligations if there was a breach of a loan-level representation and warranty.”

DBRS also noted the “relatively weak representations and warranties framework” as a potential drawback.

“Compared with other post-crisis representations and warranties frameworks, this transaction employs a relatively weak standard, which includes materiality factors, the use of knowledge qualifiers, as well as sunset provisions that allow for certain representations to expire within three to six years after the closing date,” DBRS said.

“The framework is perceived by DBRS to be weak and limiting as compared with the traditional lifetime representations and warranties standard in previous DBRS-rated securitizations.”

Additionally, nearly 64% of the underlying loans are located in California. The geographic concentration of the deal is a concern for both KBRA and DBRS.

“Compared to other recent prime jumbo securitizations, the JPMMT 2014-OAK4 pool has a high concentration of loans in California, particularly the San Francisco area with the San Francisco-San Mateo-Redwood City and Oakland-Fremont-Hayward MSAs representing about 29.7% of the pool,” DBRS said.

“Performance of loans that are highly concentrated in a particular region may be more sensitive to any deterioration in economic conditions or the occurrence of a natural disaster in that region.”

Both ratings agencies compensate for these geographic variables in the ratings methodologies.

“KBRA’s methodology to account for risks associated with geographic concentration resulted in an increase to the ‘AAA’ expected loss of 33.5% from the loan- level model results for this pool,” KBRA said.

The loans will be serviced or subserviced by RPM (19.8%), PHH Mortgage (16.6%), Dovenmuehle Mortgage (15.4%), Shellpoint Mortgage Servicing (15.2%), Homestreet (8.3%) and various other servicers, each comprising less than 5% of the mortgage loans.